The Auction Advantage

Selling distressed properties at auction provides sellers with an outcome that is more fiscally and socially responsible than selling distress on the retail market

Distressed home sales are square pegs that don’t fit well into the round hole of the retail housing market, a reality that has been highlighted by the recent economic upheaval induced by the coronavirus pandemic.

The economic upheaval has somewhat surprisingly triggered a frenzy of demand in many local housing markets as buyers clamor for a limited supply of lower-density housing far away from the madding crowd. Purchase mortgage applications rose annually for the sixth consecutive week in the week ending June 26, according to the Mortgage Bankers Association, and pending home sales in May spiked 44 percent from April, the biggest monthly increase on record, according to the National Association of Realtors.

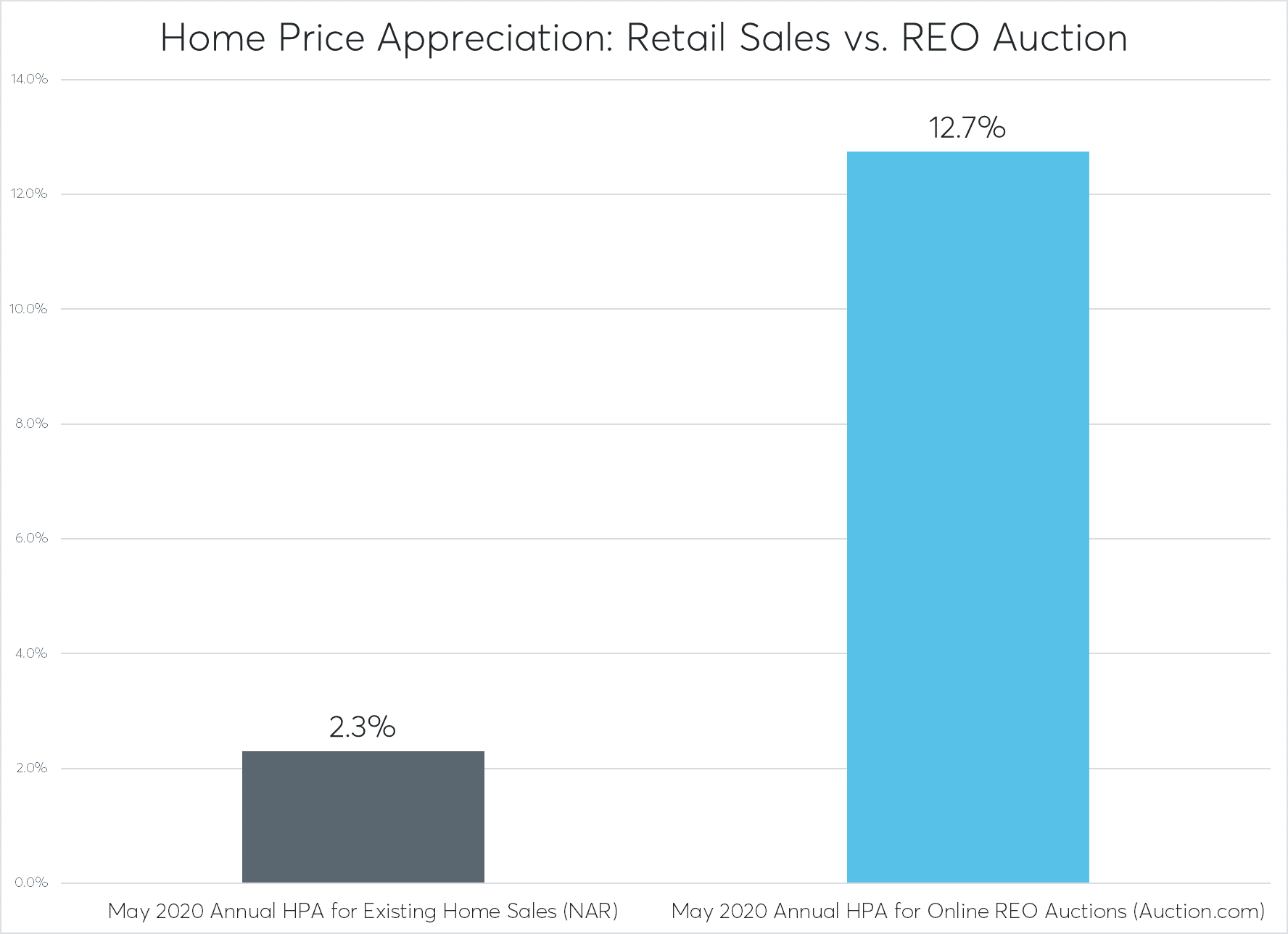

That frenzied demand coupled with muted inventory — existing home inventory was still 19 percent below year-ago levels in May — has put upward pressure on home prices in some local markets while others are suffering, resulting in mediocre home price appreciation at the national level. Median home prices nationwide increased 2.3 percent in May, according to the NAR, the lowest home price appreciation since February 2012.

Meanwhile the average sale price for bank-owned (REO) homes sold via online auction on the Auction.com platform increased 12.7 percent in May.

A More Consistently Competitive Marketplace

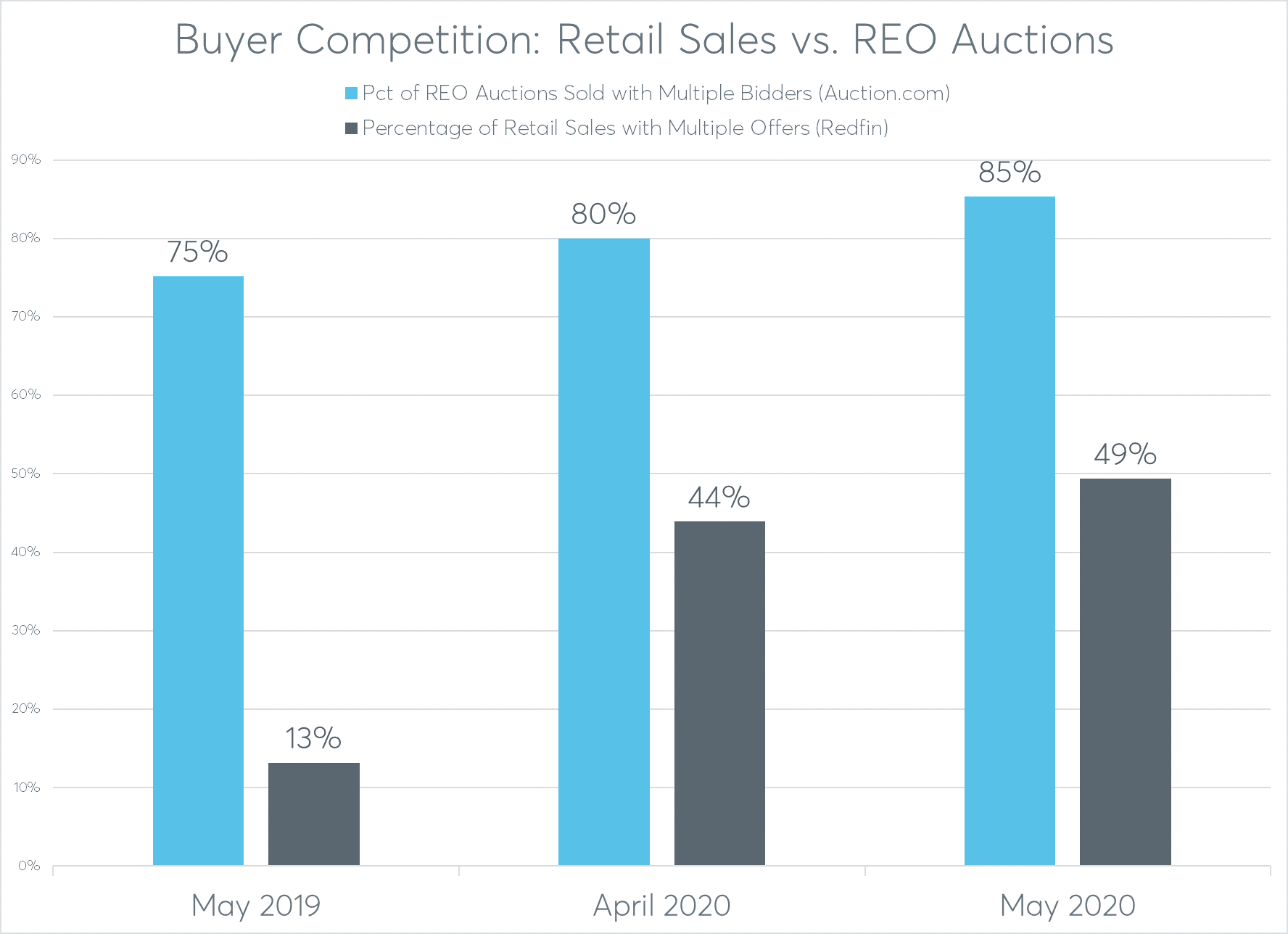

Auctions are also outperforming the retail market when it comes to buyer competition. According to Redfin, the share of MLS listings with multiple offers increased to 49 percent in May, and was above 50 percent in some markets, including Boston, Dallas, Washington, D.C., Salt Lake City, and Denver.

But even in this frenzied market, the share of retail homes with multiple offers is dwarfed by the share of multiple bidders for distressed homes sold via online auction. Proprietary data from Auction.com shows 85 percent of all bank-owned (REO) homes sold in May received bids from multiple, unique bidders — well above the retail share of 49 percent.

The share of online REO auction properties with competing bidders rose in the wake of the pandemic-induced economic crisis — similar to the trend in the retail market — but buyer competition at online auction has been much less volatile than the retail market over time. The share of multiple offers in the retail market, as measured by Redfin, dropped to a 10-year low of 9 percent in December 2019. That same month, 75 percent of REOs sold on the Auction.com platform had multiple, competing bidders.

Lower Holding Costs

The inconsistent level of competition in the retail market is especially detrimental for distressed properties that aren’t also serving as shelter or producing income for the sellers. Each day a distressed property sits on the market represents additional holding costs that aren’t providing any corresponding benefit (e.g. shelter or rental income) for the homeowner.

Additionally, each day a distressed property sits on the market represents additional risk to the seller and the surrounding neighborhood. Many distressed properties are vacant or abandoned, making them magnets for vandalism and general neglect, both of which contribute to neighborhood blight.

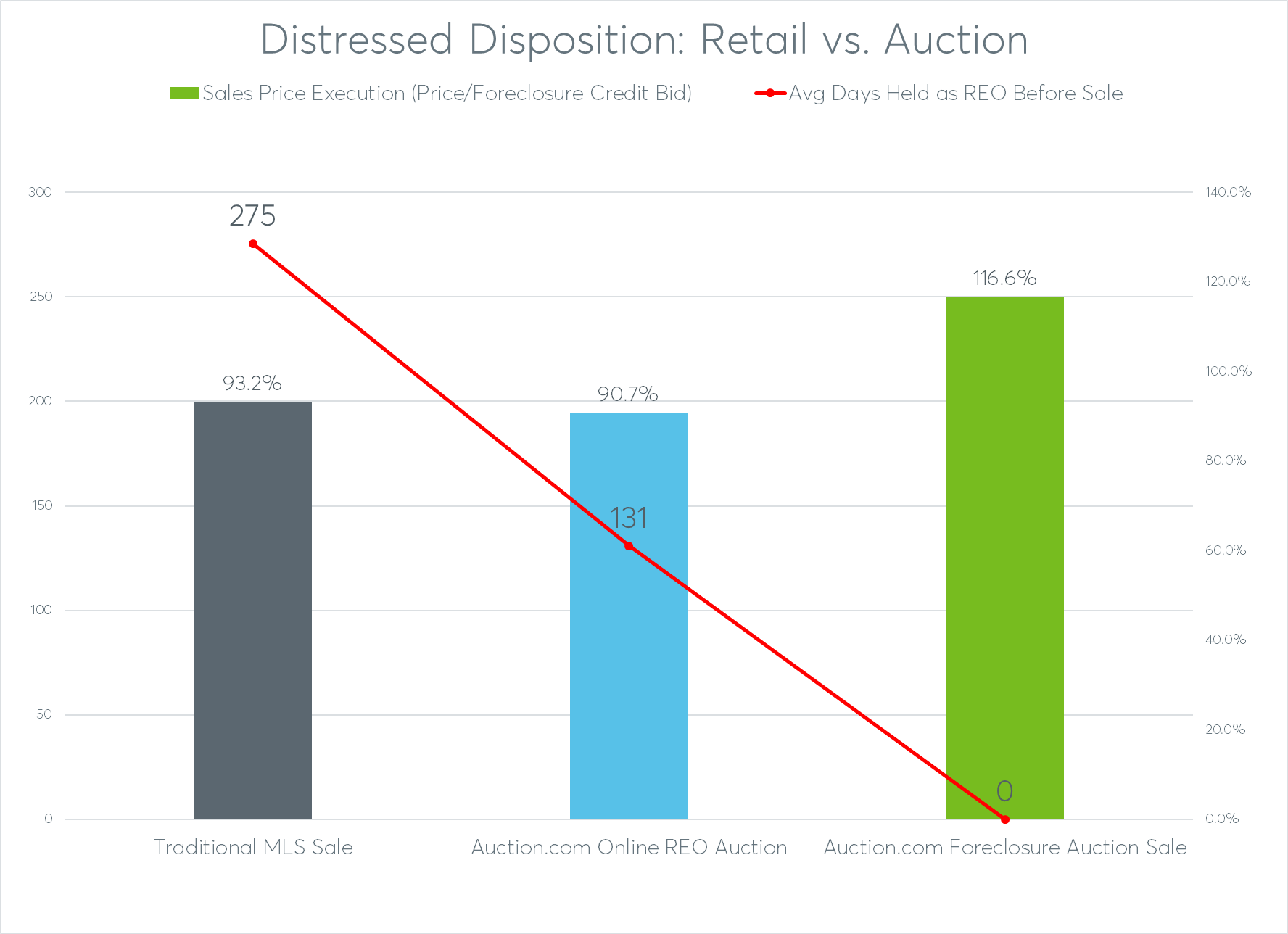

More capricious demand in the retail market results in longer days on market for distressed properties, according to an Auction.com analysis of more than 15,000 distressed property dispositions in Q4 2019 using proprietary foreclosure auction data, public record data and MLS data.

The analysis shows that REO homes sold on the MLS took an average of 275 days to sell from the completed foreclosure auction while homes that sold via online REO auction on the Auction.com platform took an average 131 days to sell after the foreclosure auction – 144 days faster than the retail market. Of course, homes that sold to third-party buyers at the foreclosure auction were not held by the mortgage servicer at all, meaning zero REO holding costs and zero REO holding risks.

Better Price Execution

Even without factoring in holding and resale costs, the Auction.com analysis found that distressed homes sold to third-party buyers at foreclosure auction performed better in terms of price execution relative to the seller’s credit bid at the foreclosure auction. Those third-party foreclosure sales sold for an average of 116.6 percent of the seller’s credit bid, while homes that reverted to REO and then resold on the MLS (275 days later) sold for an average of 93.2 percent of the seller’s credit bid set back at the foreclosure auction — without accounting for any costs associated with holding and selling the homes.

Meanwhile homes that reverted to REO at the foreclosure auction but then were sold via online auction were sold for an average of 90.7 percent of the seller’s credit bid at the foreclosure auction. Although slightly below the price execution for REOs sold on the MLS, those online auction sales closed 144 days faster on average than the MLS sales, saving servicers 144 days’ worth of holding costs.

Deciphering the Disposition Decision Tree

This all begs the question of why distressed homes sold via auction are selling faster, attracting more buyer competition and ultimately achieving better price execution relative to seller reserve than distressed homes sold on the retail market.

Auctions outperform the MLS when it comes to distressed sales for a deceptively simple reason: the inherently distressed condition of these homes tends to attract cash buyers and deter retail buyers who are using financing. This reality forces distressed property sellers into a disposition decision tree that typically ends with auction as the optimal sales method.

The inherently distressed condition of most distressed properties means that many don’t qualify for traditional financing options available to retail buyers. This gives the seller a choice to either sell as-is to a cash buyer or to renovate the property into financeable condition so it can be sold to a retail buyer.

If the property is sold as-is on the MLS, it likely won’t attract optimal competition from cash buyers because most cash buyers are looking elsewhere (i.e. at auction) to find deals. A survey of Auction.com buyers in April found that only 12 percent of buyers selected the MLS as their preferred property acquisition method compared to 61 percent who selected online REO auctions as their preferred property acquisition method.

Furthermore, the few cash buyers who are mining the MLS for deals are accustomed to getting a discount when they acquire properties through that channel. This is evident from an analysis of public record sales data from ATTOM Data Solutions, which shows all-cash homebuyers in 2019 purchased for 10 percent below estimated market value on average while homebuyers using financing purchased for 3 percent above market value on average. The analysis excluded cash buyers purchasing at foreclosure sale.

On the other hand, if a distressed property is renovated into financeable condition before it is resold, the seller (rather than a cash-buying real estate investor) takes on the risk of holding and renovating the property — betting that the renovations will ultimately help the property sell at a higher price point. It’s clear from the aforementioned price-to-credit bid ratios that this additional risk and renovation cost do little to improve price execution and can even harm price execution.

Higher Owner-Occupancy Rates

Many mortgage servicers are admirably committed to promoting neighborhood stabilization through their distressed disposition strategy. Renovating and reselling to retail buyers — who are more likely to be owner-occupants than the cash-buying real estate investors — may seem like the best disposition strategy for promoting neighborhood stabilization.

But it turns out that is often not the case.

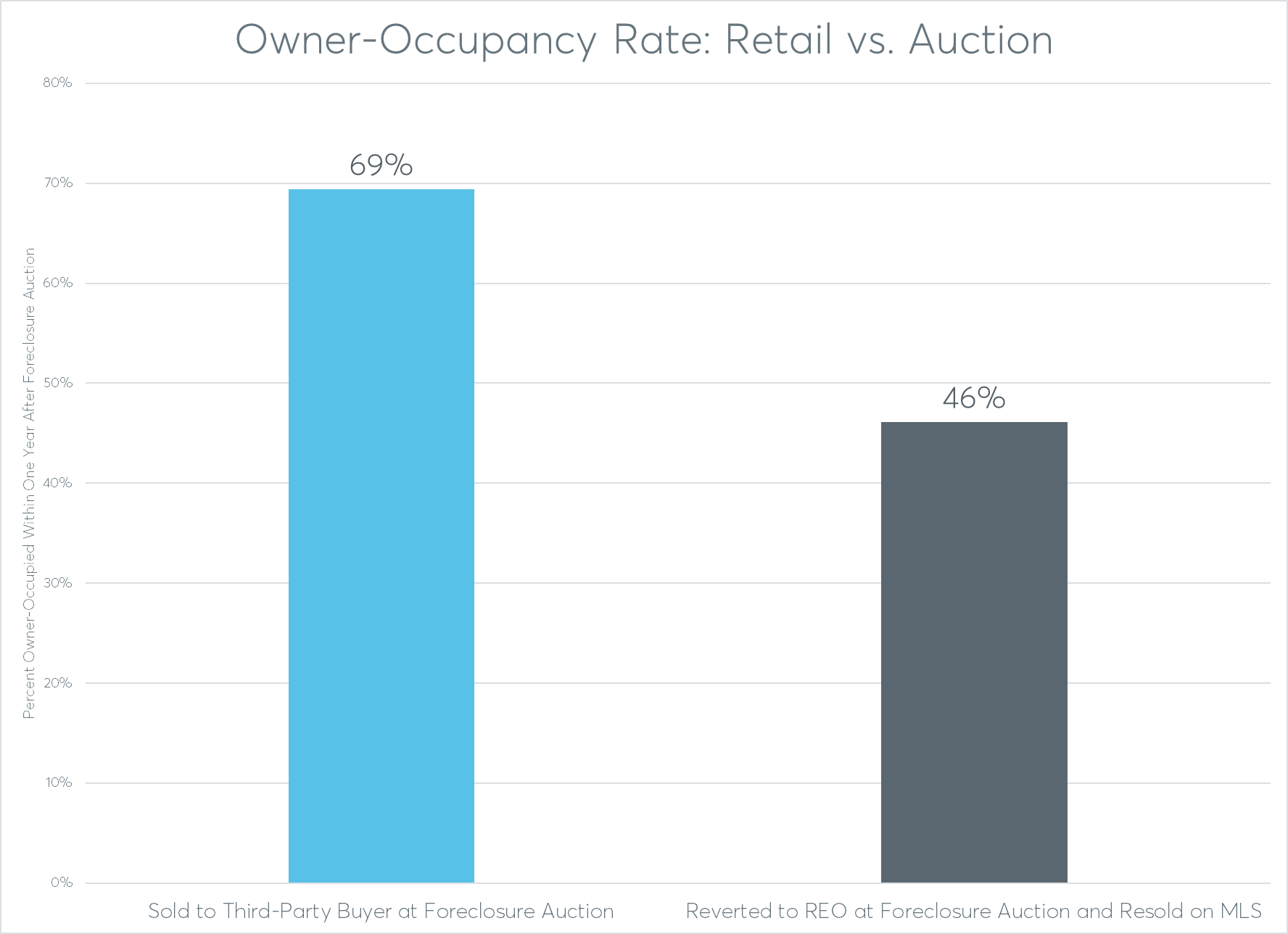

An Auction.com analysis of more than 165,000 properties brought to foreclosure auction in 2018 and 2019 found that REO properties resold on the MLS were less likely to be owner-occupied a year after the foreclosure auction than properties that sold to third-party buyers at the foreclosure auction. According to the analysis, 69 percent of properties sold to third-party buyers at the foreclosure auction (typically cash-buying investors) were owner-occupied within a year, compared to a 46 percent owner-occupancy rate for properties that reverted to REO at the foreclosure auction and then were subsequently resold on the MLS.

This analysis implies that cash-buying real estate investors are better than mortgage servicers at efficiently getting formerly distressed homes into the hands of owner-occupants.

Building Wealth Locally

Given that the majority of foreclosure auction buyers are small, often local, real estate investors — a February 2020 Auction.com buyer survey found that 76 percent of buyers purchased five or fewer properties in 2019 — selling at the foreclosure auction has the added neighborhood stabilization benefit of providing a wealth-building opportunity for local entrepreneurs who will likely invest back into the community.

“I’m looking for a way to make homes more affordable because I’ve seen these homes become more out of reach for many,” said Michael Johnston, owner of New Orleans-based Rehab2Home Properties, which buys and rehabs distressed homes, many located in low-income Opportunity Zones. Johnston grew up in the area and wants to give back to the community while building wealth. “I used to ride my bicycle through the neighborhood. … I am all for helping my community, but I can’t do it for free.”

Johnston is primarily employing the hold-as-rental investing strategy for homes located in Opportunity Zones, given that the program requires investors to hold properties for at least 10 years to receive the full tax benefit.

“If you’re willing to buy a property and hold it for 10 years or more, then the capital gains tax you would pay on a sale would actually disappear,” Johnston said, adding that he believes the neighborhoods he’s investing in could see more rapid appreciation over the next decade as a result of being designated as Opportunity Zones. “If I build (and rehab) enough homes in these areas, and other people join in, what could happen in 10 years? We’ll see.”